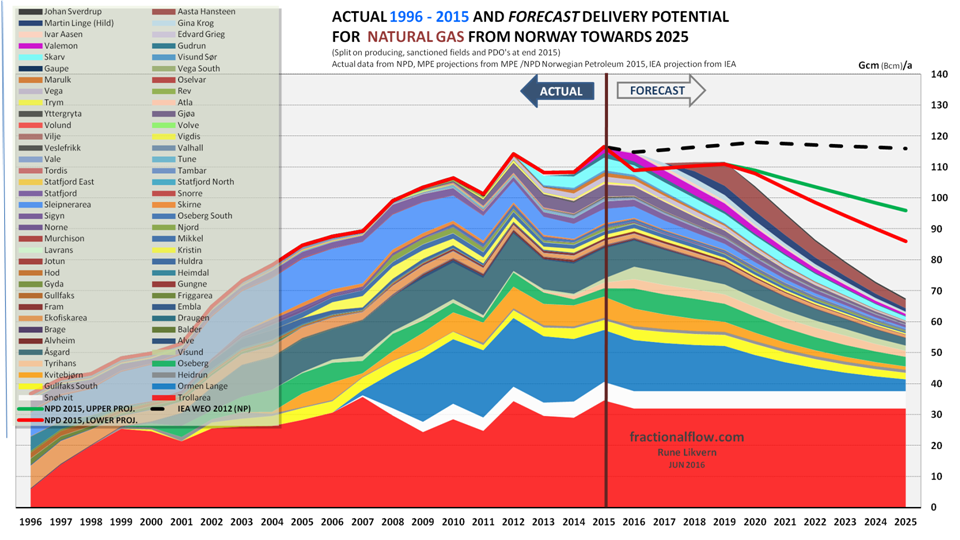

In this post I present actual Norwegian crude oil extraction and status on the development in discoveries and reserves and what this has now resulted in for expectations for future Norwegian crude oil extraction.

This post is also an update of an earlier post about Norwegian crude oil reserves and production per 2015.

Norwegian crude oil extraction peaked in 2001 at 3.12 Million barrels per day (Mb/d) and in 2016 it was 1.62 Mb/d, growing from 1.57 Mb/d in 2015 and 1,46 Mb/d in 2013 (a growth of 10% since 2013).

The Norwegian Petroleum Directorate’s (NPD) recent forecast expects crude oil extracted from the Norwegian Continental Shelf (NCS) to become 1.60 Mb/d in 2017.

Further, the chart shows a forecast for total crude oil extraction from sanctioned discoveries/fields (green area, refer also figure 02) and expected contribution from Johan Sverdrup phase I (blue area) [at end 2016 estimated at 1.78 Gb; [Gb, Giga (Billion) barrels, refer also figure 07] and this development phase is now scheduled to start flowing in late 2019.

My forecast for 2017 is 1.51 Mb/d with crude oil from the NCS.

My forecast shown in figure 01 includes all producing and sanctioned developments, but not contingent resources in the fields (business areas). The forecast is subject to revisions as the reserve base becomes revised (as discoveries pass the commercial hurdles) the tail is likely to fatten as from 2022/2023 mainly due to Johan Sverdrup phase II and Johan Castberg (Barents Sea).

My forecast includes about 7% reserve growth (300 Mb) for discoveries in the extraction phase, but does not include the effects from fields/discoveries being plugged and abandoned as these reach the end of their economic life.

Discoveries sanctioned for development and Johan Sverdrup (with an expected start up late 2019) is expected to generally slow down the decline in Norwegian crude oil extraction.

Continue reading “Norwegian Crude Oil Reserves And Extraction per 2016”

![Figure 1: The stacked areas in the chart above shows changes to crude oil supplies split with North America [North America = Canada + Mexico + US], OPEC and other non OPEC [Other non OPEC = World - (OPEC + North America)] with January 2007 as a baseline and per June 2016. Developments in the oil price (Brent spot, black line) are shown against the left axis.](https://runelikvern.com/wp-content/uploads/2020/05/2f3c2-fig-1-world-crude-oil-relative-to-jan-07.png)

You must be logged in to post a comment.