In this post I present actual Norwegian crude oil extraction and status on the development in discoveries and reserves and what this has now resulted in for expectations for future Norwegian crude oil extraction.

This post is also an update of an earlier post about Norwegian crude oil reserves and production per 2013.

Norwegian crude oil extraction peaked in 2001 at 3.12 Million barrels per day (Mb/d) and in 2014 it was 1.52 Mb/d.

The Norwegian Petroleum Directorate’s (NPD) recent forecast expects crude oil extraction from the Norwegian Continental Shelf (NCS) will become around 1.49 Mb/d in 2015.

![Figure 01: The chart shows the historical extraction (production) of crude oil (by discovery/field) for the Norwegian Continental Shelf (NCS) with data from the Norwegian Petroleum Directorate (NPD) for the years 1970 - 2014. The chart also includes a forecast for crude oil extraction from discoveries/fields towards 2040 based on reviews on individual fields, NPD’s estimates of remaining recoverable reserves, the development/forecast for the R/P ratio etc. as of end 2014. Further, the chart shows a forecast for total crude oil extraction from sanctioned discoveries/fields (green area, refer also figure 02) and expected contribution from Johan Sverdrup (blue area) [at end 2014 estimated at 2.22 Gb; [Gb, Giga (Billion) barrels, refer also figure 05] which is now scheduled to start flowing in late 2019.](https://runelikvern.com/wp-content/uploads/2020/05/c0089-figure-01-actual-and-forecast-crude-oil-production-for-norway.png)

Further, the chart shows a forecast for total crude oil extraction from sanctioned discoveries/fields (green area, refer also figure 02) and expected contribution from Johan Sverdrup (blue area) [at end 2014 estimated at 2.22 Gb; [Gb, Giga (Billion) barrels, refer also figure 05] which is now scheduled to start flowing in late 2019.

My forecast for 2015 is 1.47 Mb/d with crude oil from the NCS.

My forecast shown in figure 01 includes all sanctioned developments and not discoveries (refer also figure 07) and contingent resources in the fields. The forecast is subject to revisions as the reserve base becomes revised (as discoveries pass the commercial hurdles) which likely will fatten the tail post 2020 of the presented forecast.

My forecast assumes some reserve growth, but does not include the effects from fields/discoveries being plugged and abandoned as these reach the end of their economic life.

Discoveries sanctioned for development and Johan Sverdrup (with an expected start up late 2019) is expected to slow down the decline in Norwegian crude oil extraction.

The forecast in figure 1 shows that the Norwegian crude oil extraction will be in a general decline in the coming decades. Norwegian oil consumption is now around 0.2 Mb/d, and with what is known about Norwegian crude oil reserves, Norway will be a net exporter of crude oil for another 20 to 30 years.

Discoveries under development and scheduled to start to flow during 2015 – 2017

Presently it is expected that around 0.08 Mb/d (Mb; Million barrels) on an annual basis will be added during 2015 from start ups of sanctioned developments.

Norway extracted, sold and delivered around 554 Mb of crude oil in 2014. Sanctioned developments are now estimated to add around 750 Mb of crude oil reserves for extraction for the years 2015 – 2017.

Some developments/discoveries are reported under other business areas and are included in these.

My 2014 forecast

In the spring of 2014 I forecast that crude oil extraction from NCS in 2014 would become 1.44 Mb/d and it became 1.52 Mb/d. The reasons for this deviation are several.

The condensates from fields in the Sleipner area were reclassified to crude oil as of April 2014 and became part of what is referred to as Gudrun blend. These contributed around 13 kb/d for all 2014.

kb/d; kilo (1,000) barrels per day

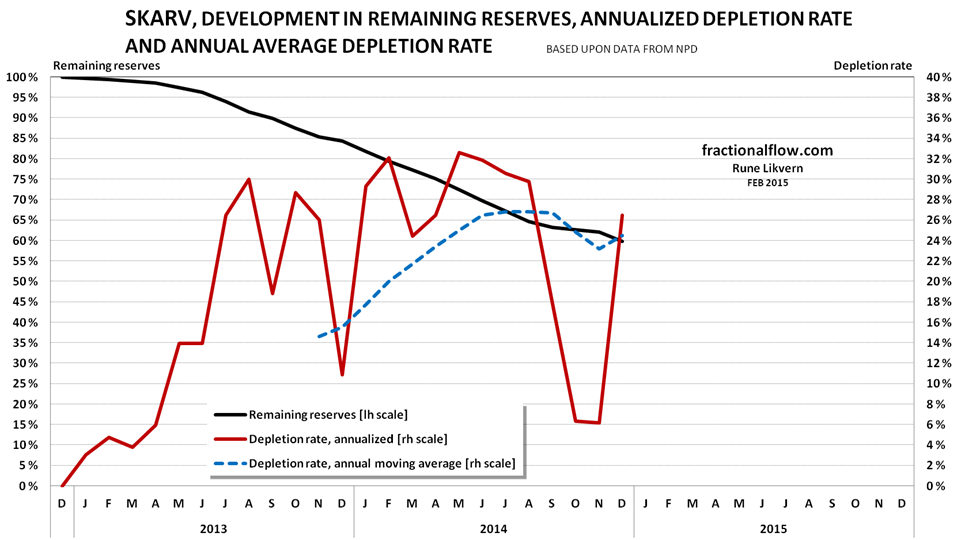

Crude oil extraction from Skarv, refer also figure 11, was higher than modeled which partly was offset from deferred start up of Goliat (In the Barents Sea), adding net around 20 Kb/d.

Several of the older legacy fields like Ekofisk, Snorre, Troll, Valhall (new installations) and Visund increased their total extraction with around 40 kb/d from 2013 to 2014.

The above describes most of the deviations from my 2014 forecast, refer also figure 03.

The high oil price has likely allowed for more profitable infill drilling in legacy fields.

A closer look at actual crude oil extraction

Note the recent years slow down and temporary reversal in crude oil extraction from discoveries starting to flow prior to 2002.

In 2014 around 60% of the crude oil flow was from discoveries that started to flow prior to 2002.

There is reason to believe that the high oil price in recent years allowed for more infill drilling. Infill drilling allows both for accelerated depletion and increased recovery. Inasmuch as infill drilling has been widely used in recent years, a period with significantly lower oil prices may materialize itself through higher decline rates.

The characteristics of “small” deepwater discoveries/fields (here defined as having less than 100 Mb of recoverable crude oil) are a fast build up, followed by a short plateau (typically 2 years) succeeded by steep declines, typically at annual rates of 15 – 20%, refer also figures 11 and 12.

Several of the recent NCS developments, after the increase in the oil price, has been subject to both considerable write downs (which weakens the companies’ balance sheets and thus affect their financial capacities for future investments) and downward revisions to the estimates of recoverable reserves.

Development of Norwegian crude oil reserves

(Gb; G = Giga, Billion barrels)

Figure 05 illustrates that the biggest NCS discoveries were made early and these discoveries continues to contribute a big portion of total NCS crude oil production.

Figure 05 also illustrates that the growth in the oil price above $50/bbl in 2005 and its structurally higher level allowed for increased exploration activities resulting in several successful discoveries with the most prominent being the Johan Sverdrup discovery in 2010.

The chart above is based upon NPD’s resource accounting at end 2014.

![Figure 06: The chart above shows the development of total NCS crude oil discoveries since exploration began and as of end 2014 [data from NPD Resource Accounting at end 2014]. The chart is often referred to as a “creaming curve”. The light green portion of the columns shows the development in total extracted, sold and delivered. The dark green portion shows the development in estimated remaining recoverable reserves. The yellow portion shows the development in total estimated reserves in discoveries that has not been sanctioned at end 2014. Johan Sverdrup is presently included in the yellow portion of the columns.](https://runelikvern.com/wp-content/uploads/2020/05/d23be-figure-06-norway-crude-oil-creaming-curve-and-developments-of-reserves.png)

The light green portion of the columns shows the development in total extracted, sold and delivered. The dark green portion shows the development in estimated remaining recoverable reserves. The yellow portion shows the development in total estimated reserves in discoveries that has not been sanctioned at end 2014. Johan Sverdrup is presently included in the yellow portion of the columns.

![Figure 07: The chart above shows NCS discoveries in various evaluation phases, their estimated recoverable crude oil reserves versus year of discovery. In the chart is also shown development in the nominal oil price (Brent). Green circles: Resource Category 4F, in planning phase. Yellow circles: Resource Category 5F, development likely, but not clarified. Pink circles: Resource Category 7F, not evaluated. NOTE; For reasons of scaling Johan Sverdrup (which Plan for Development and Operation [PDO] is in process) and Johan Castberg in the Barents Sea and above 72 degrees North (both Category 4F) are not shown.](https://runelikvern.com/wp-content/uploads/2020/05/0d977-figure-07-norway-crude-oil-discoveries-and-their-reserves.png)

In the chart is also shown development in the nominal oil price (Brent).

Green circles: Resource Category 4F, in planning phase.

Yellow circles: Resource Category 5F, development likely, but not clarified.

Pink circles: Resource Category 7F, not evaluated.

NOTE; For reasons of scaling Johan Sverdrup (which Plan for Development and Operation [PDO] is in process) and Johan Castberg in the Barents Sea and above 72 degrees North (both Category 4F) are not shown.

Due to scaling the chart does not include Johan Sverdrup and Johan Castberg (Barents Sea).

The green dots represent discoveries closest to passing the commercialization hurdle.

High oil and natural gas price are likely required to commercialize these discoveries with possible startups in the next decade.

The R/P ratio reveals the future trajectory for NCS crude oil extraction

A simplistic description of the R/P ratio (Reserves at year end divided by the Production for that same year) is the (theoretical) number of years the extraction/production level may be sustained using that year as a baseline. In the real world it works somewhat differently, as the reservoir depletes the extraction will (normally) decline. This may result that the R/P ratio remains fairly constant during the decline/tail phase as the reservoir depletes and the extraction declines.

![Figure 09: The chart above shows cumulative NCS crude oil extraction versus the fields/discoveries R/P ratio in the extraction phase at end 2014 plotted against the right hand scale [black dots connected by a black line]. The red line, plotted against the left hand scale, shows the cumulative portion of the crude oil extraction versus the R/P ratio.](https://runelikvern.com/wp-content/uploads/2020/05/c8afe-figure-09-norway-crude-oil-extraction-versus-r-over-p-ratio.png)

Figure 09 illustrates that above 50% of the NCS crude oil extraction in 2014 was from 47 fields/discoveries with an R/P ratio of 6 or less. The weighted R/P ratio for these 47 fields was 3.9 at end 2014, refer also figure 10. This suggests that the total year over year decline from 2014 to 2015 may become above 20% or more than 0.15 Mb/d due to decline from depletion of these 47 fields.

Around 10% of the NCS crude oil extraction in 2014 came from discoveries/fields with an R/P ratio above 14.

Broadly speaking reservoirs with an R/P ratio of less than 6 for crude oil should be expected to experience declines in extraction, and year over year declines in the range of 15 – 20% has been observed. Discoveries/fields with R/P above 6 has some potential to increase extraction if these are not reservoir and/or facilities constrained (processing, transport etc).

The crosses in the chart show the weighted R/P ratio and average estimated remaining recoverable crude oil reserves (per discovery/field) for the described ranges.

Discoveries/fields that both have a high (above 6) R/P ratio and a meaningful amount of recoverable reserves, have in theory potential for a meaningful increase in extraction.

As figure 10 shows those discoveries/fields with some potential for meaningful increases in extraction (yellow and green dots) are long in their teeth and past their prime several years ago.

To summarize my forecast/expectations for NCS crude oil extraction in 2015;

I showed further up (refer figure 02) that additions in 2015 from sanctioned developments are forecast to add 0.08 Mb/d and fields with R/P ratios below 6 are forecast to decline around 0.15 Mb/d, which leaves the discoveries/fields with an R/P ratio above 6 to offset the remaining balance of 0.07 Mb/d in decline, this if extraction levels in 2015 shall become equal to 2014 (1.52 Mb/d).

Depletion and depletion rates

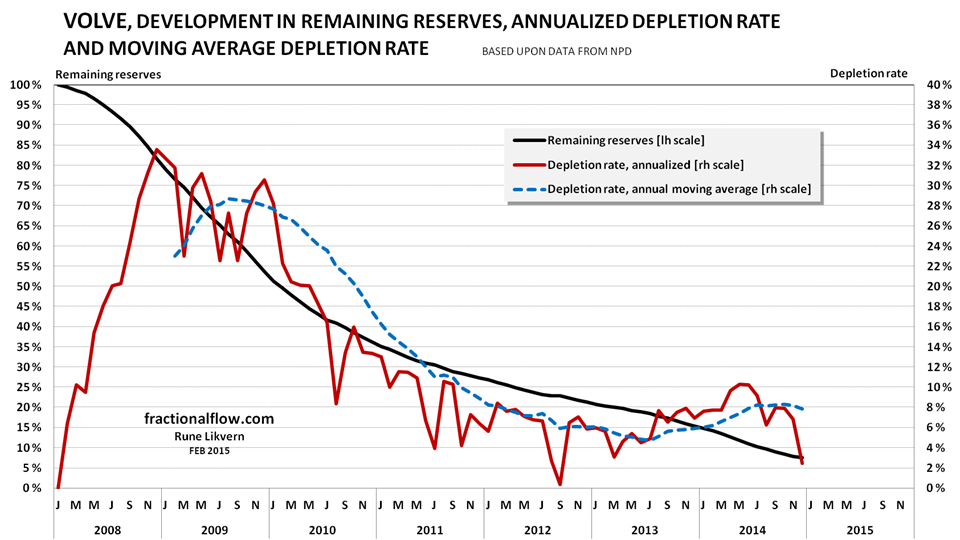

A closer look at the depletion of two deep water fields show the rapid depletion and high decline rates, which are common in such discoveries/fields with about 100 Mb of recoverable crude oil.

At end 2014 NPD estimated Skarv to have contained 86 Mb with original recoverable crude oil.

The past high crude oil depletion rate for Skarv suggest now a steep decline for the near future extraction.

At end 2014 NPD estimated Volve to have contained 61 Mb with original recoverable crude oil.

From 2009 to 2011 the observed year over year decline in extraction for Volve was somewhere between 40 – 50%.

In general and with oil prices above $100/Bbl the oil companies’ net cash flows and profits was, and have been struggling from bringing the more expensive barrels to the market. It appears the oil companies, encouraged by the prospects from a sustained high oil price, assumed more debt to go after the costlier oil. This was likely rooted in the expectations that consumers would continue to assume more debt and/or draw down their savings to afford the higher price that would ensure the oil companies’ return requirements and health of their balance sheets.

The recent collapse in the oil price hurt the oil companies’ cash flows, returns and balance sheets, prompting all along the line drastic cut backs to their near and medium term capital expenditures (CAPEX) in pursuit of maintaining dividend payments to please the investors, improve financial performance and strengthen their balance sheets.

In general, future developments of discoveries on NCS require a high breakeven price (above present oil price of $60/Bbl) and the effects of the oil companies’ CAPEX reductions will affect the pace of developments of discoveries and infill drilling (may affect contingent resources) under evaluation and thus both future total NCS investments and extraction developments.

You must be logged in to post a comment.