The saying is that hindsight (always) provides 20/20 vision.

In this post I present a retrospective look at my prediction from 2012 published on The Oil Drum (The “Red Queen” series) where I predicted that Light Tight Oil (LTO) extraction from Bakken in North Dakota would not move much above 0.7 Mb/d.

- Profitable drilling in Bakken for LTO extraction has been, is and will continue to be dependent on an oil price above a certain threshold, now about $68/Bbl at the wellhead (or around $80/Bbl [WTI]) on a point forward basis.

(The profitability threshold depends on the individual well’s productivity and companies’ return requirements.) - Complete analysis of developments to LTO extraction should encompass the resilience of the oil companies’ balance sheets and their return requirements.

![Figure 01: The chart above shows development in Light Tight Oil (LTO) extraction from January 2009 and as of August 2014 in Bakken North Dakota [green area, right hand scale]. The top black line is the price of Western Texas Intermediate (WTI), red middle line the Bakken LTO price (sweet) as published by the Director for NDIC and bottom orange line the spread between WTI and Bakken LTO wellhead all left hand scale. The spread between WTI and Bakken wellhead has widened in the recent months.](https://runelikvern.com/wp-content/uploads/2020/05/128f7-figure-01-bakken-oil-production-and-oil-prices-august-2014.png)

LTO extraction in Bakken (and in other plays like Eagle Ford) happened due to a higher oil price as it involves the deployment of expensive technologies which again is at the mercy of:

- Consumers affordability, that is their ability to continue to pay for more expensive oil

- Changes in global total debt levels (credit expansion), like the recent years rapid credit expansion in emerging economies, primarily China.

- Central banks’ policies, like the recent years’ expansions of their balance sheets and low interest rate policies

- Credit/debt is a vehicle for consumers to pay (create demand) for a product/service

- Credit/debt is also used by companies to generate supplies to meet changes to demand

- What companies in reality do is to use expectations of future cash flows (from consumers’ abilities to take on more debt) as collateral to themselves go deeper into debt.

- Credit/debt, thus works both sides of the supply/demand equation

- How OPEC shapes their policies as responses to declines in the oil price

Will OPEC establish and defend a price floor for the oil price?

I have recently and repeatedly pointed out;

- Any forecasts of oil (and gas) demand/supplies and oil price trajectories are NOT very helpful if they do not incorporate forecasts for changes to total global credit/debt, interest rates and developments to consumers’/societies’ affordability.

Oil is a global commodity which price is determined in the global marketplace.

Added liquidity and low interest rates provided by the world’s dominant central bank, the Fed, has also played some role in the developments in LTO extraction from the Bakken formation in North America.

As numerous people repeatedly have said; “Never bet against the Fed!” to which I will add “…and China’s determination to expand credit”.

Let me be clear, I do not believe that the Fed’s policies have been aimed at supporting developments in Bakken (or other petroleum developments) this is in my opinion unintended consequences.

In Bakken two factors helped grow and sustain a high number of well additions (well manufacturing);

- A high(er) oil price

- Growing use of cheap external funding (primarily debt)

In the summer of 2012 I found it hard to comprehend what would sustain the oil price above $80/Bbl (WTI).

The mechanisms that supported the high oil price was well understood, what lacked was documentation from authoritative sources about the scale of the continued accommodative policies from major central banks’ (balance sheet expansions [QE] and low interest rate policies) and as important; global total credit expansion, which in recent years was driven by China and other emerging economies.

I have described more about this in my post World Crude Oil Production and the Oil Price.

Summer of 2012

With oil prices at the wellhead in Bakken at $70/Bbl in the summer of 2012, the companies netted back around $45/Bbl.

In the summer of 2012 monthly LTO extraction was on its way towards 19 million barrels (Mb).

The total monthly net cash flow from the LTO extraction generated thus about $850M ($45/Bbl X 19 Mb) which could fund monthly additions of 85 – 95 wells (if the companies’ cash flows unabridged was used for well manufacturing).

This level of well manufacturing was estimated to sustain an LTO extraction level of 0.7 Mb/d in Bakken(ND).

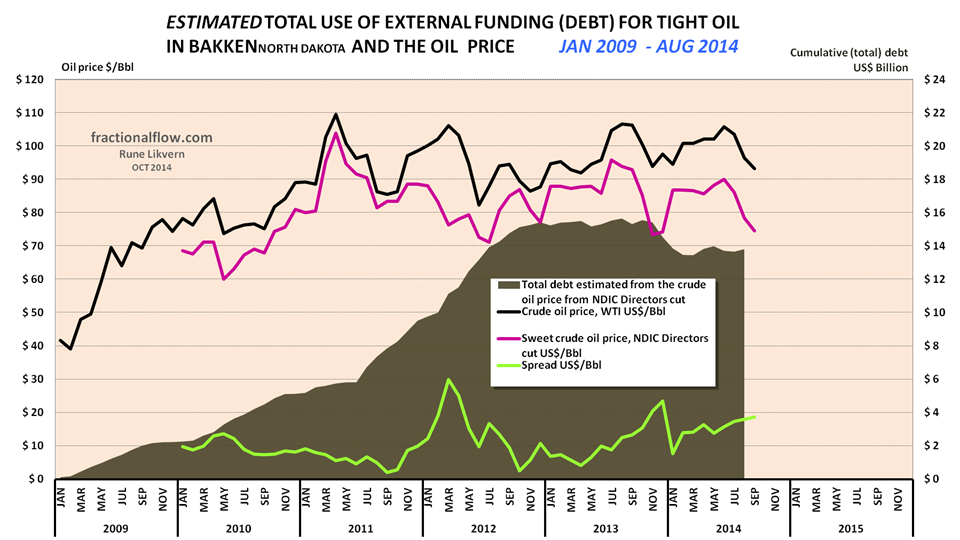

The companies had, by then and based on a low end estimate, added a total of $14 Billion in external funding, primarily debt, refer also figure 03.

Summer of 2014

The assumptions for the chart are WTI oil price (realized price which is netted back to the wellhead), average well costs starting at $8 Million in January 2009 and growing to $10 Million as of January 2011 and $9 Million as of January 2013. All costs assumed to incur as the wells were reported starting to flow (this creates some backlog for cumulative costs as these are incurred continuously during the manufacturing of the wells) and the estimates do not include costs for non- flowing and dry wells, water disposal wells, exploration wells, seismic surveys, acreage acquisitions etc.

Economic assumptions; royalties of 16%, production tax of 5%, an extraction tax of 6.5%, OPEX at $4/Bbl, transport (from wellhead to refinery) $12/Bbl and interest of 5% on debt (before any corporate tax effects).

Estimates do not include the effects of hedging, dividend payouts, retained earnings and income from natural gas/NGPL sales (which now and on average grosses around $3/Bbl).

Estimates do not include investments in processing/transport facilities and externalities like road upkeep, etc. The purpose with the estimates presented in the chart is to present an approximation of net cash flows and development of total use of primarily debt for manufacturing of LTO wells.

The chart serves as an indicator of the cash flow for the aggregate of oil companies in Bakken.

Since the fall of 2012 and until the summer of 2014 oil prices at the wellhead in Bakken oscillated around $90/Bbl (ref also figures 01 and 04) which netted back around $60/Bbl to the companies.

This makes a material difference to the companies’ net cash flows from LTO extraction and they also added an estimated $2 Billion (low end estimate) in debt since the summer of 2012. The companies had thus considerably improved their abilities to fund growth for and sustain a high level of (monthly) well additions which provided for growth in LTO extraction.

In the summer of 2014 monthly LTO extraction was on its way towards 32 Mb.

The total monthly net cash flow from the LTO extraction generated thus about $1,900M ($60/Bbl X 32 Mb) which unabridged could fund monthly additions of 190 – 210 wells (no dividends paid out and/or down payments of debt). This is close to the number of monthly well additions reported by NDIC since the harsh winter loosened its grip.

Note in figures 03 and 04 how the (low end) estimates for total debt has more or less remained flat since last winter.

Now (fall 2014)

In the chart is also shown the developments in the oil price WTI (black line), at the wellhead (dark red line) and the spread between WTI and the wellhead price (light green line), all left hand scale.

Since last summer world oil prices have come significantly down and I hold it likely they will remain low or decline some more if not OPEC curtails its supplies. As of writing the wellhead price in Bakken is $63/Bbl (sweet and as of Oct. 30th) and the “average” point forward breakeven is estimated at $68/Bbl (at a 7% discount rate and at the wellhead).

The effect of the low oil price causes a noticeable reduction in companies’ total netted cash flows which now is estimated below $1,400M/month.

This ($63/Bbl at the wellhead) cash flow could unabridged fund 140 – 155 wells/month.

However the world does not work as straight forward as this.

Companies in Bakken had levered up (used debt) likely under the expectations that oil prices would remain high(er). It was the expectations of sustained high cash flows that (primarily) was/is used as collateral to assume more debt. Various covenants may dictate the companies to continue to manufacture wells. A higher leverage (from declining cash flows) results in relative higher debt carrying costs.

A lower oil price shrinks the debt potential on their balance sheets and some will deleverage (reduce their total debt) as a response to the lower oil price.

Their sources of income to reduce their debt; a portion of their cash flows from their operations and/or sales of assets.

The dividend policies vary amongst public companies and oil companies have been facing mounting pressures from impatient investors who looks for yield.

For public companies, there has been an additional powerful factor at play after the Fed started QEing, key phrase: Companies’ Market Capitalisation, refer also figure 10.

Investors in companies involved in LTO extraction had no reason to complain as there was growth in LTO extraction and QE “buoyed everything” with little relation to the actual underlying fundamentals.

My model (also presented in the “Red Queen” series at The Oil Drum) estimates it now takes around 130 net well additions/month in Bakken (ND) to sustain present LTO extraction levels. This could be funded with a wellhead price around $60/Bbl, if the companies’ net cash flows unabridged were spent towards well manufacturing.

However the financial capacities of the companies becomes impaired from a sustained lower oil price and these will start deleveraging, thus reducing their capital expenditures which, and with a time lag, entail a down scaling of their well manufacturing.

This change in strategy is often presented under the euphuism of “targeting financial performance”.

If monthly net well additions drop below the “Red Queen” number (now estimated at 130 – 135 wells/month), Bakken(ND) LTO extraction is likely to decline.

A sustained lower oil price, thus:

- Impairs the companies’ abilities for well manufacturing (reduces funding from cash flows)

- Drives the need for deleveraging (which reduces the funds which otherwise could be allocated towards well manufacturing)

- May give priorities to complete wells that are drilled, but not completed as there exists a big inventory of wells drilled and not completed and funding for the completions comes from the cash flows. These wells represent “cheap” flow additions.

The LTO Break Even Price

Another parameter which is important to keep an eye on is the development to the break even price that meets the companies’ return expectations. The wells come with individual designs (costs), flow rates and EURs and the break even price is subject to a range of return requirements [my presented numbers are discounted at 7%].

I have used actual well data from North Dakota Industrial Commission (NDIC) to make estimates of what I will continue to refer to as the “reference/average well”, refer also figure 07.

Since I started following the Bakken LTO developments this “reference/average well”, and notably since 2013, has experienced some improvements to its total first 12 months cumulative LTO extraction (refer also figure 07) and the judges are still out there if the deployment of improved (and likely more expensive) technologies allows for some faster extraction and/or increased total extraction (higher EURs).

Changes in the oil price are the dominant source for changes to the financial returns of the wells.

Those who does not worry about returns (that is a discount rate at 0% of full life cycle costs) would now achieve this with around $50/Bbl at the wellhead.

Who are willing to put their money at risk for a 0% return? (Putting the money in the mattress gives the same return.)

A sustained oil price below $70/Bbl (at the wellhead) is, with a time lag, likely to slow drilling activities as this is the profitability threshold for the “average” well. Should the oil price (at the wellhead) remain below $70/Bbl the oil companies will focus on drilling those wells expected to meet their return requirements. If wells meet their expectations is not known before after it has flowed for several months.

One early indicator for changes in activity levels is to follow the development of the number of rigs drilling.

Well productivity Developments

Longer laterals, more use of proppants, more fracking stages, has with time lead to documented improvements in well productivity (here defined as total LTO extracted during the first 12 months of flow) for the “average” well in the Bakken formation in North Dakota, refer also figure 07.

More advanced wells may, however, mask the possibility of extraction growth from areas with poorer geology.

Developments as of Aug 2014

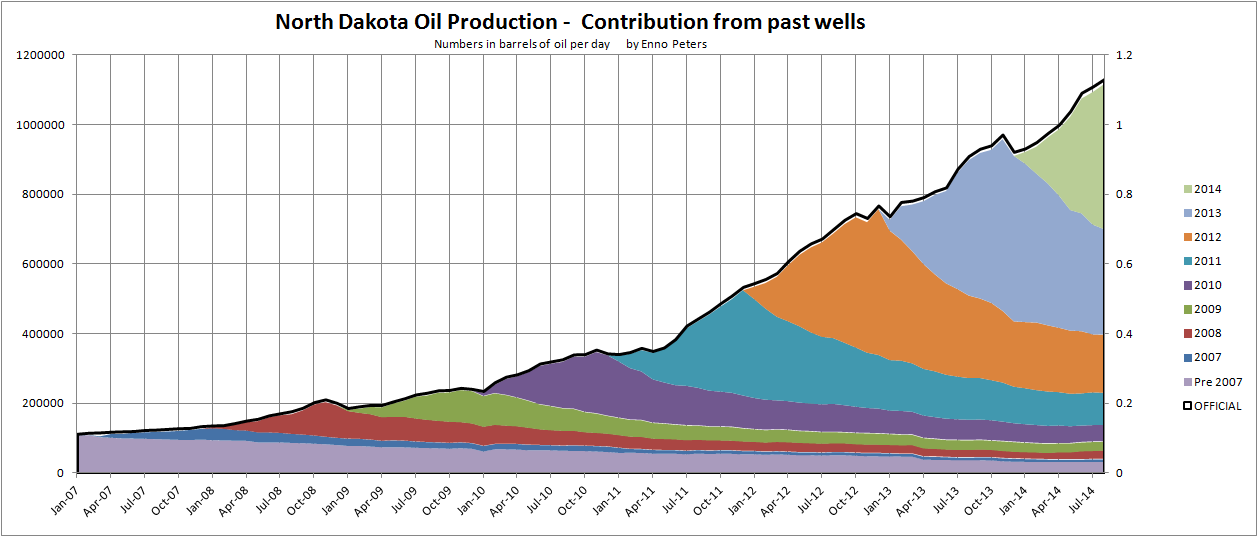

Three of the charts below have expertly been produced and provided by Enno Peters, who agreed to let me use them in this post.

Chart by Enno Peters.

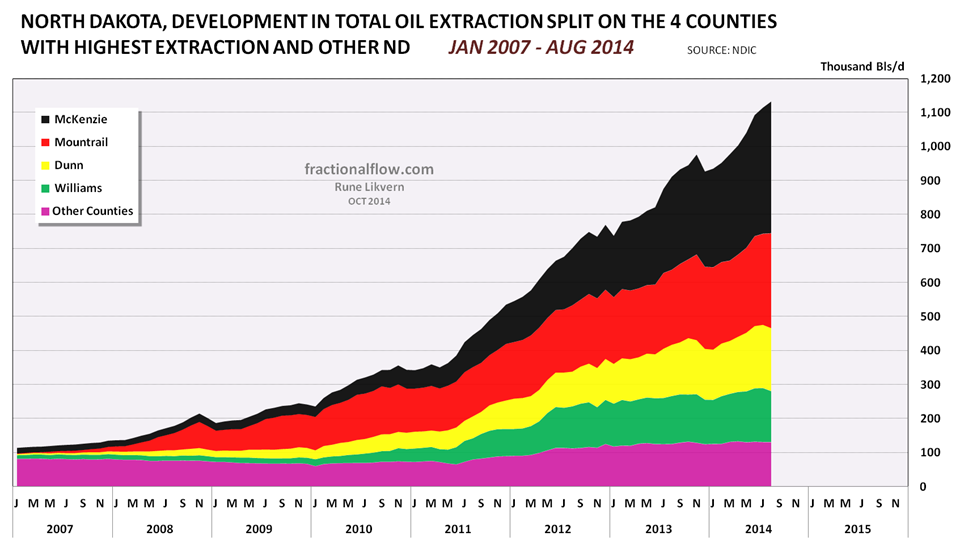

The strong growth in LTO extraction happened while the wellhead price in Bakken was above $70/Bbl, refer also figure 01.

![Figure 06: The chart above, based upon the NDIC data for figure 05, shows how LTO extraction in Bakken declines by vintage [end of year].](https://runelikvern.com/wp-content/uploads/2020/05/e1f38-figure-06-bakken-decline-by-vintage.png)

This illustrates that LTO as a source of sustained oil supplies requires to stay on the drilling treadmill. The LTO extraction level is sensitive to the oil price, the companies’ return requirements and the strength of their balance sheets.

![Figure 07: The chart above shows how cumulative LTO extraction for the “average” well by vintage [calendar year] develops with time. Chart by Enno Peters.](https://runelikvern.com/wp-content/uploads/2020/05/78e8b-figure-07-bakken-total-lto-extraction-by-well-and-vintage.png)

Chart by Enno Peters.

Total Extracted Liquids from Bakken Wells has grown with time, led by Produced Water

![Figure 08: The chart above shows development in the water to oil ratio for the “average” wells by vintage [calendar year] in Bakken. Produced water (brine) is separated and transported to dedicated disposal sites. Chart by Enno Peters.](https://runelikvern.com/wp-content/uploads/2020/05/0d19f-figure-08-bakken-water-to-oil-ratio-by-vintage.png)

Chart by Enno Peters.

Some Supplementary Information

To me what we are now witnessing is the most telegraphed correction in history. The end of Fed’s QE and higher Fed’s fund rates in the near future.

I will briefly present two macroeconomic sizes that helped sustain a high oil price.

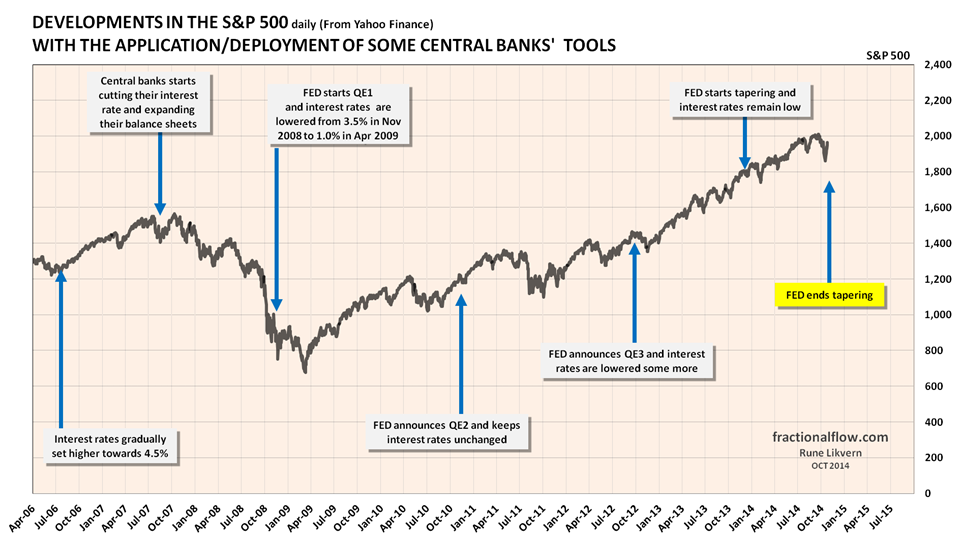

![Figure 09: The chart above shows the developments in the oil price [Brent spot; black line and WTI; red line] and the time of the Fed’s announcements/deployments of available tools to support the global financial markets which the economy heavily relies upon. The financial system is virtual and thus highly responsive. The chart suggests causation between Fed policies and movements to the oil price.](https://runelikvern.com/wp-content/uploads/2020/05/1af37-figure-09-the-oil-price-and-application-of-fed-policies.png)

The chart suggests causation between Fed policies and movements to the oil price.

The chart suggests causation between Fed policies and movements in the stock index.

Several of the listed companies active in LTO extraction are included in the S&P 500 index, thus these were given an uplift from the general bull market and investors in LTO saw their share prices rise.

The common features of figures 09 and 10 are that they show possible causations from Fed’s policies. Added liquidity and low interest rates also supported the oil price and the stock market.

![Figure 11: The chart above shows [left panel] how advanced economies’ central banks in concerted efforts lowered their interest rates following the Global Financial Crisis (GFC) in 2008. The middle panel shows the relative growth (expansion) of the balance sheets (assets) for US Federal Reserve (Fed), European Central Bank (ECB), Bank of England (BoE) and Bank of Japan (BoJ) post the GFC. Note the growth of the Fed’s balance sheet since 2012 (middle panel). The right hand panel shows the development in long and short term interest rates together with the twenty year average. Chart from p 24 in BIS 84th Annual Report, 29 June 2014.](https://runelikvern.com/wp-content/uploads/2020/05/712df-figure-11-advanced-economies-central-banks-balance-sheets-and-interest-rates.png)

The middle panel shows the relative growth (expansion) of the balance sheets (assets) for US Federal Reserve (Fed), European Central Bank (ECB), Bank of England (BoE) and Bank of Japan (BoJ) post the GFC. Note the growth of the Fed’s balance sheet since 2012 (middle panel).

The right hand panel shows the development in long and short term interest rates together with the twenty year average.

Chart from p 24 in BIS 84th Annual Report, 29 June 2014.

So what about China?

Oil is a global commodity. China has in recent years had strong economic growth, which has been facilitated by a rapid credit expansion. This has allowed China to steadily grow its oil imports and consumption (refer also figure 14), which thus supported growth in global oil demand and a higher oil price.

Figure 12 has been lifted from p 70 of the Geneva 16th report “Deleveraging? What Deleveraging?” made public 29 September 2014.

Note the rapid growth in Chinese debt post 2008 in figure 12 and note the growth in Chinese petroleum consumption and imports since 2008 in figure 14. China continued good economic growth post the GFC by aggressive credit expansion.

According to data from the Bank for International Settlements (BIS in Basel, Switzerland) China saw its annual growth rate in private, non financial sector debt accelerating from around 10 Trillion Yuan as of Q4 2010 to 18 Trillion Yuan (about US$3 Trillion) as of Q1 2014. (100 Yuan approximates USD 16)

The Shift in Oil Consumption

![Figure 13: Chart above (areas are not stacked) shows developments in OECD total petroleum consumption (grey area), production (green area) and net imports (red area) since 1965 and as of 2013 [rh scale] together with the oil price [Brent, black dots and lh scale].](https://runelikvern.com/wp-content/uploads/2020/05/d72eb-figure-13-oecd-oil-consuption-production-and-net-imports.png)

- The oil price has in recent weeks significantly weakened and if a higher demand/consumption within OECD fails to materialize from this weakness, this strongly suggests influences from other structural forces.

![Figure 14: The chart above (areas are not stacked) shows developments in China’s total petroleum consumption (grey area), production (green area), net exports (blue area) and net imports (red area) since 1965 and as of 2013 [rh scale] together with the oil price [Brent, black dots and lh scale].](https://runelikvern.com/wp-content/uploads/2020/05/e3eea-figure-14-china-oil-consumption-production-net-imports-and-exports.png)

Summary

The spectacular growth in LTO extraction in Bakken in the recent years happened because of a sustained high(er) oil price and the use of more cheap debt for funding. Now it appears this development nears a crossroads.

LTO developments are flexible and allow for rapid adaptation to changes in the oil price and each well represents limited capital requirements, as opposed to large capital intensive oil developments that takes years to bring on line.

It normally takes 4 to 6 months from a LTO well is spudded until it starts to flow.

The prices at the wellhead in North Dakota is now around $63/Bbl (sweet) and should oil prices remain low (or go lower), the future developments of LTO extraction in Bakken will move into the twilight zones between profitability (return requirements), reduced capital expenditures (from declines in cash flows which shrinks the companies’ debt capacities), deleveraging, dividend policies and OPEC policies.

It is from this twilight zone the Bakken “Red Queen”, for some time outrun by the high oil price, cheap debt funding, growth in global total debt and low interest rates will emerge and catch up.

From here it will be most interesting to follow the continued race between Bakken LTO extraction and its “Red Queen”.

Another well-researched article. Thanks.

It could well be killing two birds with one stone strategic orchestrated move; to demotivate/dampen shale oil production (or other sorts of higher-cost alternative oil production), which protects conventional oil producers’ market share. As you said, once it breaks/disconnects the feedback mechanism in shale oil business will, in due time, collapse should oil price remain at this level or lower. Lower crude price can also add negotiating power in political bargaining with Russia and Iran.

BTW, Where can you find spot Bakken wellhead price?

LikeLike

How much changes in the oil price is due to concerted political efforts I know little about.

It is MHO that this is the workings of several structural forces (finance/monetary/total debt levels/austerity measures/affordability issues…to name some).

Monthly data on Bakken oil price are from NDIC Directors Cut.

Daily from Plains.

LikeLike

Sorry this is OT, but Peak Water. Peter Gleick thinks that the newly released USGS data on water usage in the U.S. is a success story for innovation and efficiency: http://scienceblogs.com/significantfigures/index.php/2014/11/05/peak-water-united-states-water-use-drops-to-lowest-level-in-40-years/

But it looks to me like a standard depletion curve, esp. given the rapid increases in the price of water (http://water.epa.gov/action/importanceofwater/upload/19-Maxwell.pdf). What do you think?

LikeLike

I appreciate your work. Thank you for providing it online to the public. I am interested in how you determine “average” EUR for wells in the Bakken area of North Dakota. I note the chart provided to you by Enno Peters which shows greater “early” production in recently drilled wells, but that they converge with the earlier drilled wells over time. I am particularly interested in how long Bakken wells will continue to be economic at various oil price points. Although I have done nothing scientific, just by observing many production histories, it appears that the wells’ decline curves flatten out considerably when they reach 20-60 bbl per day range. Also, it appears “average” EUR may be skewed upward considerably by a few “sweet spot” areas, such as Parshall. If you have a previous post where you have discussed these issues, please let me know. Thank you.

LikeLike

Hello and thank you.

There are several discussions running about the “fat” tails for LTO wells and how well the Arp’s equation is suited to predict future flows from shale oil wells.

All of theses exercises, try to establish a good EUR number (after 20 – 30 years of flow) which as of now is educated guesses. So are mine (and I am very much aware of it).

That is also the reason why I do not focus much on estimating EUR numbers (and relate to actual data and how these may trend).

To me what to focus on are the financial dynamics of production and then understanding the NPV curve at several discount rates.

The companies operating in LTO are doing it to turn a profit (wealth creation).

It will all be educated guesses to now try to predict how long a LTO well has positive cash flow (the oil price and flow are the major variables).

Let me try to illustrate this with a theoretical example.

A well has over 4-5 years of flow reached a level of 50 b/d.

If this well from now on declines at an average rate of 10% annually it would take around 16 years before it reached a level of 10b/d. (A lower decline rate leads to a slower decline and a higher decline rate a faster decline and this also affects the EUR for the well).

For an early entrant the physical flow 20 years down the line has little effect on the company’s NPV for the well (I am treating each well as a project), even though the well may have, call it a decent flow after 20 years, show a healthy net cash flow, it barely moves the NPV figure as NPV is all about getting the money (flow) as early as possible. This example well would produce a total of around 150 kb as illustrated from reaching 50 b/d down to 10 b/d.

For wells, where there are actual data on, it turns out that they reach a level of about 50 b/d after 4 to 5 years.

For the wells in Bakken with actual data, these shows that they on average has a total/cumulative after 4-5 years of around 170 kb.

Based on earlier work on Bakken my estimates for the average well suggested and EUR of 300 kb +/- 10% (LTO and exclusive of natural gas and NGLs).

More than 2 years down the line and tons of additional actual data has not and as of now given the support for that the average EUR number is due for revision.

I have the NDIC data and capabilities to sort wells by the pools (Alger, Parshall, Sanish, etc.) and also by operating companies. Admittedly it takes some time to run through such an exercise, and it has been done for a few pools and companies.

LikeLike

Thank you for your response. It would seem that if they are at, on average 170,000 cumulative in 4-5 years, they will not have paid out in that time, even ignoring present value calculations. Assuming $9-10 million to drill and complete, as reported recently by some of the companies operating there, they are looking at a payout date well in excess of 5 years with wellhead prices in the high 50/ low 60 range. I am assuming 20% royalty, $10 per bbl in LOE and severance taxes. I am not sure of effect of income taxes, but assume most IDC’s are taken early on.

I have no experience with shale production but do have with conventional production. It seems to me that if the simple calculation I have made is close, once wells already committed to are online, further development must slow. Although dry holes are uncommon in shale, there is enough variance to cause those investing in these areas to look for alternatives given there is not much reward for the risk undertaken.

Again, thank you for your website and posts. I was directed here by reading your posts on Peakoilbarrel.

LikeLike